Japan remains the single-largest country weight in the MSCI All Country World ex US Small Cap Index. However, the country’s weak economic growth, aging population, tight labor conditions, and chronic deflation have long made it a challenge to find high-quality, growing companies there.

Government regulators and the Tokyo Stock Exchange recently introduced a flurry of reforms aimed at improving corporate governance and shareholder returns. As discussed in our fourth quarter 2023 report, these actions have primarily benefited the cheapest stocks, given that they are typically associated with the least-profitable and slowest-growing companies. Additionally, the Bank of Japan has raised short-term interest rates, ending its decade-long era of negative rates. This landmark move boosted Japanese value stocks in the first quarter, further exacerbating the region’s style headwinds.

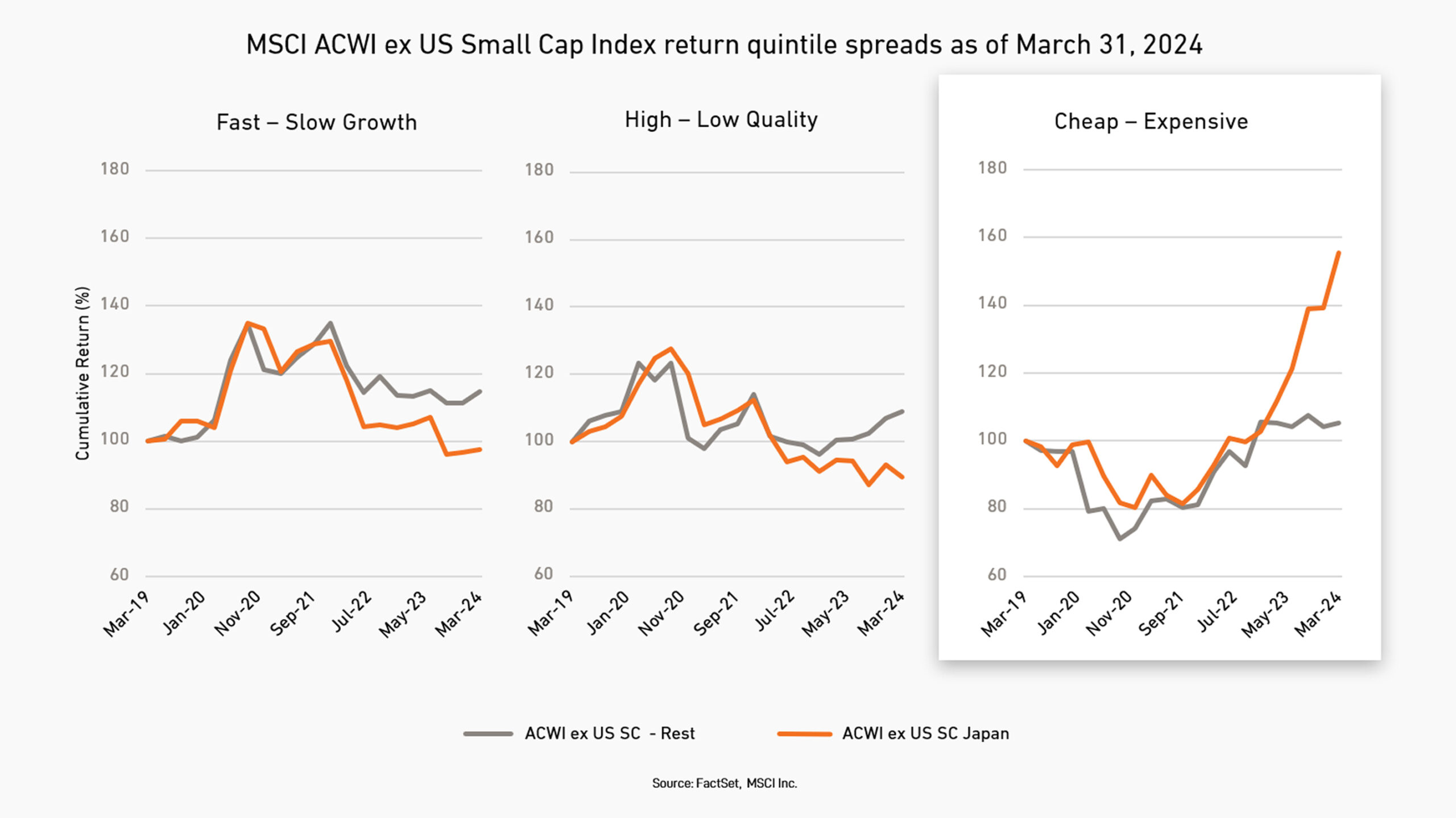

As the chart above to the right shows, the cheapest stocks in Japan outperformed the most expensive by nearly 1,600 basis points in the first quarter. For the trailing 12-month period, it’s worse: The spread between the most expensive and cheapest quintile was nearly 46%. The left and center charts show that investors also have favored slower-growing and lower-quality companies.

We don’t know how long this value rally will persist. In the short run, some of the changes have clearly exacerbated, and could prolong, style headwinds for higher-quality, faster-growing companies. But over the long term, the changes in Japanese business policy and mindset are positive developments. As more businesses raise their standards, the number of high-quality companies in Japan may increase.

What did you think of this piece?