Over the last 14 years, a powerful narrative around the exceptionalism of US equity markets took root. Dominant tech stocks, prolonged low interest rates, and economic stability led to higher returns for US stocks and caused many investors to question the necessity of international allocations. However, the tide has shifted in 2025; international equities have outperformed. Watch Portfolio Specialists Ray Vars, CFA, and Apurva Schwartz discuss the recent shift in market leadership and what the next decade might hold for global equity markets.

The transcript, lightly edited for clarity, follows.

Ray Vars: Amidst a lot of the market turmoil this year, I think something that stands out is non-US stocks outperforming the US. A lot of things today rhyme with the last time international embarked on an extended period of outperformance back in 2001: We had just come off the 1990s, a decade of US stocks outperforming, powered by great businesses, great innovation, the internet, all rooted here in the US. Earnings were strong.

We also saw the dollar strengthen for a decade, a couple hundred basis points per year. We saw a big valuation gap open up between US and non-US companies. I recall people saying, “Well, that’s okay. Why bother investing overseas? All the great businesses are here. The US is different.” But, of course, right when everybody decided that, the US went nowhere for a decade and international outperformed.

A lot of things today rhyme with the last time international embarked on an extended period of outperformance back in 2001.

Today, it feels very similar. We’ve had 14 years now of US outperformance driven by great businesses, innovation, and more earnings here. The dollar’s been strengthening for a decade and you see that valuation gap widen again, once again excused by US exceptionalism. Why bother with international companies? All the great businesses are here.

This peaked following the election last year. People said, “Oh wow! The US is going to continue to do well. The dollar’s going to strengthen.” Then we get to this year. Amidst the uncertainty, all of a sudden we’ve seen US stocks fall, international stocks actually go up, and we’ve seen the dollar weaken. The last time we saw the dollar weakening and US stocks falling was back in 2001. The question today is can we continue to see international stocks outperform over the next few years. Let’s walk through some of the reasons we think that might happen.

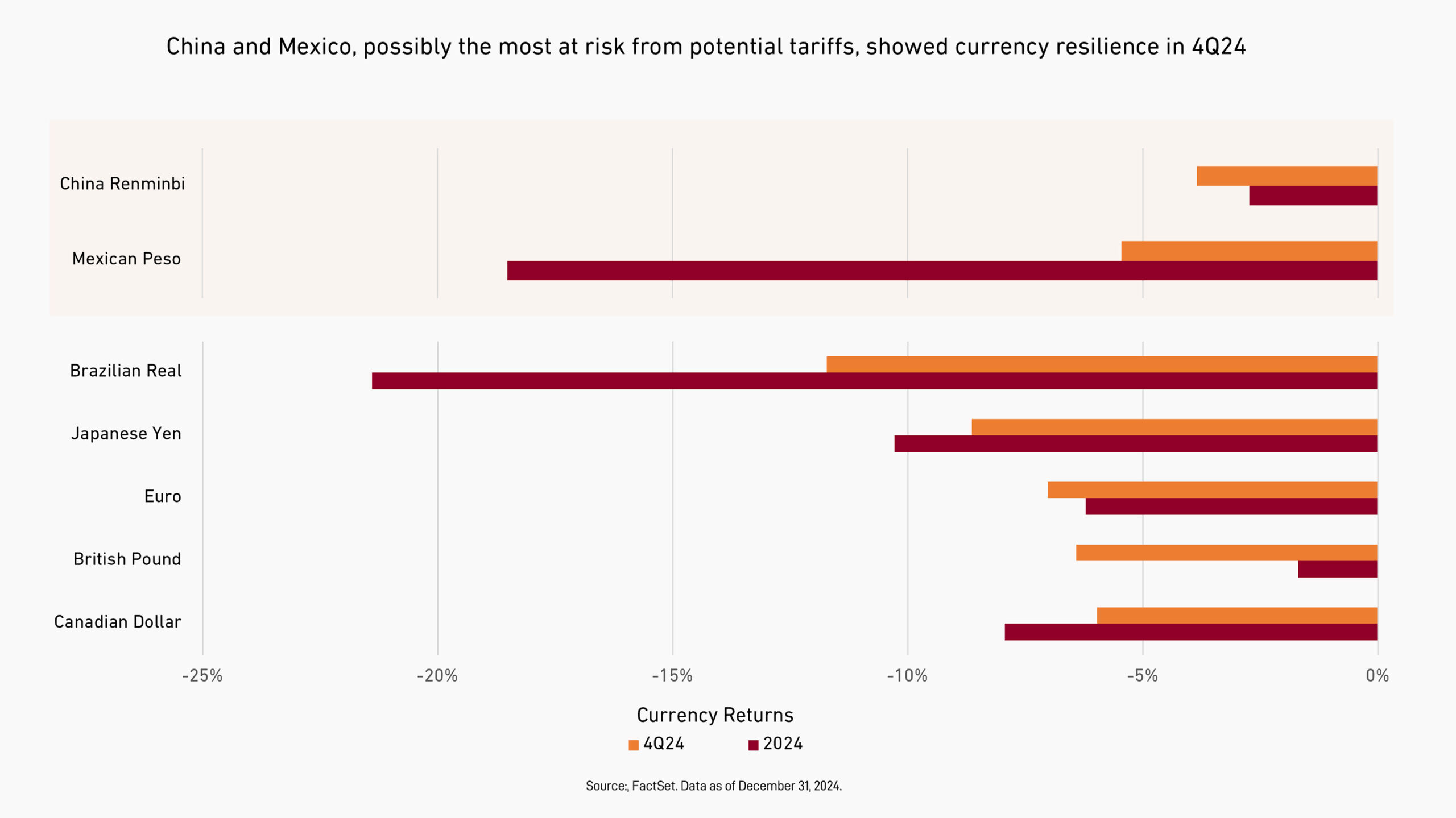

Apurva Schwartz: Maybe the first thing to talk about is tariffs. We don’t know what the policy will look like, it seems like there are changes every day, but I think tariffs are bad. Bad for companies outside the US and bad for US companies and their potential competitiveness abroad. Globalization has been such a tailwind for the US, for China, but also the world. The wealth effect and the prosperity that’s been generated by companies and countries being cooperative with each other. Interestingly enough, when you look at the last several years and the impact of the first round of tariffs we saw five or six years ago, global trade continues to do well.

Source: Deutsche Bank, Haver Analytics. Reproduced with permission.

Data depicted is IMF DOT export data for last twelve months ending September 2024 compared to the twelve-month period ending September 2017.

Current coverage of world trade represented herein is around 87%. Chart is from the report “Five Fresh Perspectives on Global Trade”

issued December 12, 2024.

I think the question is that as the US pursues a policy of tariffs, and you see retaliatory tariffs on top of that, what does that actually mean?

If global trade is continuing to do well, perhaps you are starting to see the US begin to squander that leading position that it has.

RV: That’s another interesting point, that the global leadership the US has shown—stability of policies, stability of institutions, driving for that change—I think is part of what underpins that idea of US exceptionalism and the premium valuation awarded to some US stocks, why the US dollar is the reserve currency for the world, and also why the dollar has been so strong.

To the extent that there’s some uncertainty around those things and some abdication of that leadership, it feels like that could also be a positive for non-US stocks. You can have that valuation premium evaporate a bit for the US. You could also see what we’ve been seeing today, the dollar continue to weaken.

AS: I think that’s exactly right. If you think about the enthusiasm over Europe today and the outperformance of European markets, it may be as much about people moving away from the US as it is about some changes that are happening in Europe. You have more unity, less regulation going forward, more investment as countries like Germany relax their fiscal constraints, and more monetary support.

The narrative is changing a little bit. Previously Europe was seen as slow moving, bureaucratic, and the European Central Bank behind the Federal Reserve in decision making. Now it feels that Europe is a little bit more on its front foot these days.

When you bring that to the company level, you mentioned this idea of US exceptionalism and the best businesses are found in the US, I acknowledge that earnings growth in US companies has generally been a little bit better, but The Magnificent Seven are very much a double-edged sword today. They drove the concentration of market returns in the US in 2024. But there’s certainly been a reversal of that and the pain in the markets in the US today is quite acute.

RV: Some of that reversal, if we think back over this year, is when DeepSeek announced how strong and how efficient and effective its model was. That news was certainly a shot across the bow of US-based hyperscalers, but I think it also highlights that there is innovation beyond the US.

Even within AI, when we think about who makes all of NVIDIA’s chips, TSMC makes all of them. And what equipment do they use to make it? It’s all from ASML and their extreme ultraviolet lithography (EUV) equipment. Both are near monopolies from a Taiwanese company and a Dutch company. Even the inputs are less well known, like a company called Disco in Japan: They slice, dice, and polish the wafers that are used in making those chips, and have something like a 70% market share. This is a critical niche component to the whole infrastructure and AI supply chain. Again, these are non-US companies.

When we think about who makes all of NVIDIA’s chips, TSMC makes all of them. And what equipment do they use to make it? It’s all from ASML and their extreme ultraviolet lithography (EUV) equipment. Both are near monopolies from a Taiwanese company and a Dutch company.

Even outside of tech, you’ve got a company like Schneider Electric based in France. They do energy management equipment and services and software around that. People thought about it for green energy, but the reality is they’ve got a fantastic and fast-growing business helping build out AI infrastructure. Those AI data centers need very efficient and consistent power, and I think it’s grown to something like 20% of their business from almost nothing not too many years ago.

Health care is another area of innovation outside of the US. Anti-obesity, weight loss drugs have certainly been a focus of markets and the Health Care sector. Novo Nordisk, the Danish company, is the leader. They’re competing today with Lilly. When we look forward, what people are looking for is not just the weight loss but convenience and a better safety profile with fewer side effects.

Lilly has taken to phase three a once daily oral GLP-1 drug. That would certainly be more convenient. But interestingly, the science behind that is from Chugai, a Japanese-based company. And when we think about lower side effects, Roche recently did a deal to co-develop drugs with Zealand, a Danish-based company. It’s still an injectable, but far fewer side effects than Ozempic, Wegovy, and Mounjaro. Again, a lot of innovation for future growth is coming from non-US Health Care companies.

AS: That’s a really good point. When you look at the top 20 cash-flow return-on-investment businesses, you mentioned areas of innovation like Health Care, Information Technology, and Industrials, but there are other sectors as well. You do see a preponderance of high-quality, growing businesses in those sectors outside the US.

If you look at the ACWI benchmark, the US has a large weight, 67% in US and 33% in International. But when you slice it by market cap and look at the number companies greater than US$5 billion in that high-quality growth universe, it’s a very different skew: 73% of the companies in that high-quality growth universe are outside the US. Certainly the monopoly on innovation does not belong to the United States.

RV: Yet it’s still not reflected in valuations. You see the widest gap we’ve seen in 20 plus years, actually ever I think, but it feels like that could close. We’ve listed quite a few different potential positives. If any one of them happen, it feels like that could narrow that gap and lead to some international outperformance, hopefully within rising markets.

It can also be a powerful defense. Diversification in international, if things are going awry, that valuation can provide some support in down markets, along with the quality growth of the businesses. Outperforming in down markets is actually almost more powerful than on the way up. If you think about the magic of math, if a stock falls in half, it has to double to get back to zero.

So international markets could outperform on the way up, but there’s also a good chance that they could provide protection if markets get difficult in the coming years.

AS: That point on downside protection is a good one. I also think it’s worth mentioning, from a style perspective, that growth and value have had very different experiences outside of the US, and growth stocks in the last three years have significantly underperformed to the tune of thirty percentage points unannualized versus value stocks.

To the extent that you’re looking about at international markets and looking where to put that that marginal dollar, I think international growth stocks are pretty interesting right now.

RV: Yes, I think so, too. I think international markets definitely have the potential to perform well over the coming years.