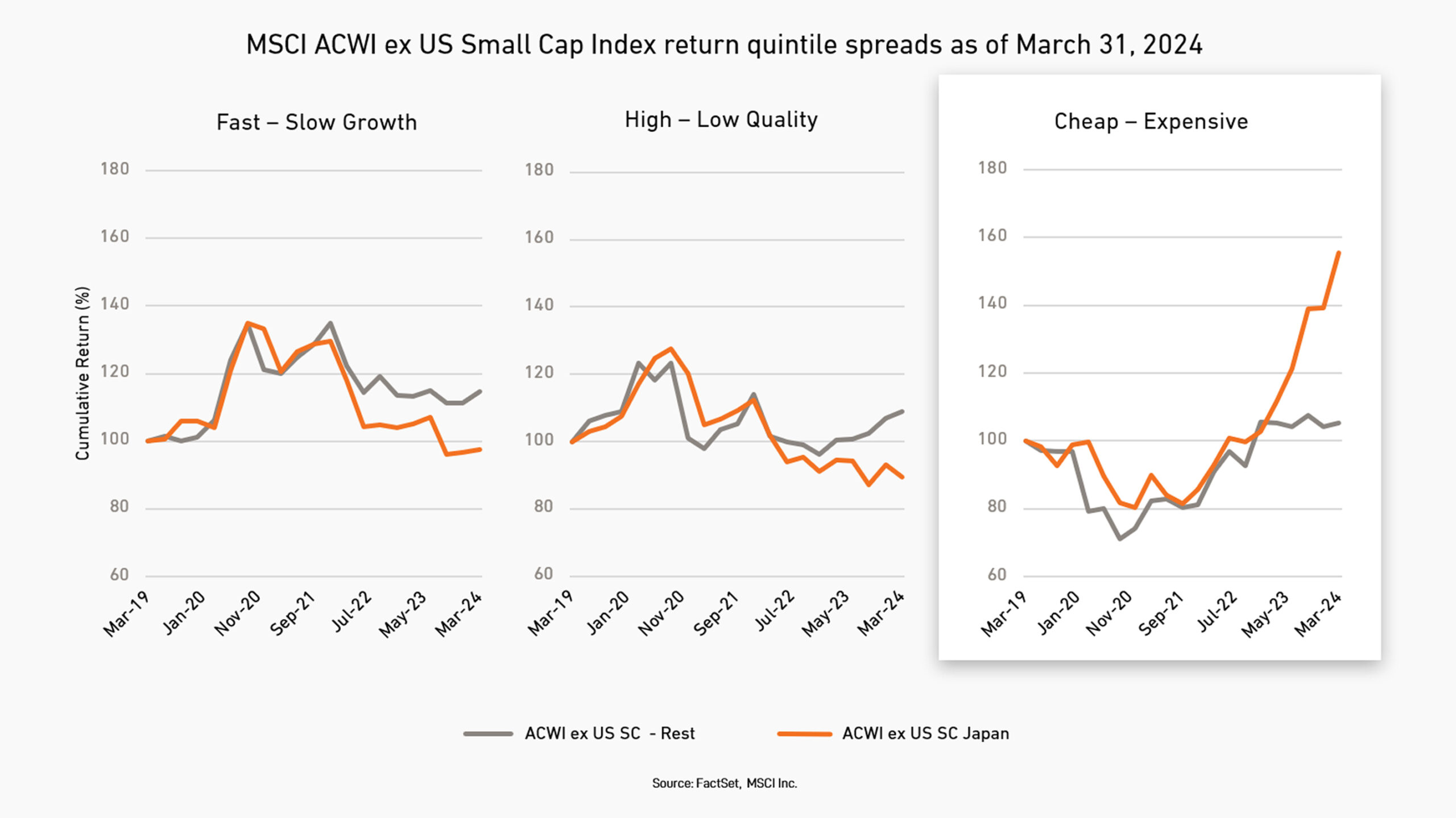

Examining the 1.2% gain of the MSCI All Country World ex US Index in the second quarter, the biggest style effect is evidenced in Japan where there continues to be a strong bias in favor of cheaper stocks, which outperformed the most expensive stocks there by nearly 700 basis points (bps). That brings the advantage for cheaper stocks over more expensive stocks, which tend to be higher-growth and higher-quality companies, to a 1,500bp difference year to date.

As we’ve explored previously, the performance of certain factors can shift markedly in just a few years. Time will tell if this value rally gives way to better performance for more expensive, higher-quality, faster-growing companies in Japan.

Outside of Japan, there didn’t appear to be strongly defined style patterns. The heatmap above shows that there weren’t consistent headwinds or tailwinds when examining performance by measures of quality, growth, and value. There did, however, appear to be a style divergence between regions.

In the Eurozone, the fastest-growing stocks performed in line with the slowest-growing stocks. In emerging markets, the concentration effect of heavyweight stocks, including TSMC and Tencent, flattered the returns of the highest-quality, fastest-growing cohorts, even while cheaper stocks outperformed. In Asian markets excluding Japan, the most expensive stocks only modestly outperformed the least expensive this past quarter. ∎