For generation after generation, hydrogen has been considered the clean energy source of tomorrow. But until very recently, the long-running joke was that it might just stay that way.

Because of game-changing regulatory developments around the world, most notably the US Inflation Reduction Act (IRA) passed in 2022, environmentally friendly production of hydrogen is no longer a theoretical solution, as pressure builds on businesses to move away from fossil fuels. Green hydrogen, the kind that is produced from water and renewable electricity, is normally very expensive to make, store, and distribute, and not to mention dangerous—more prone to igniting than even gasoline or natural gas. But these new government-provided financial incentives are starting to chip away at the cost-related challenges, enough for some companies to finally take steps toward building the early infrastructure needed to eventually produce green hydrogen on a large scale.

Green hydrogen won’t be a cure-all for the planet. For example, it’s unlikely that most people will ever live in hydrogen-heated homes or drive hydrogen-propelled vehicles. But it could be a viable alternative in certain business settings, such as high-polluting industries that are difficult to electrify—difficult because they rely on fossil fuels as a key input to create the chemical reactions at the center of their production processes. These processes also require very high heat for sustained periods, which is more easily achieved with high-density energy sources like fossil fuels and hydrogen than with electricity.

Over time, the list of possible applications for green hydrogen may expand, but in the meantime, we’ve identified some areas where innovation is happening today.

Heavy Industry

About 70% of direct industrial emissions, or one-sixth of overall manmade carbon emissions, come from a small group of manufacturers: makers of iron, steel, cement, and chemicals.

Their participation is necessary to meeting the commitment at the core of the international treaty known as the Paris Agreement, which is to limit earth’s warming to 1.5 degrees Celsius this century. To achieve this goal, the world’s greenhouse gas emissions need to be reduced to effectively zero by 2050.

Unlike other businesses, these sectors are among the largest carbon emitters because they rely on large amounts of coal, the dirtiest fossil fuel, as feedstock.

For example, to make steel, iron first must be extracted from iron ore, which is done by heating the mineral substance to extremely high temperatures in a blast furnace. This energy-intensive process typically entails burning coal, which serves a dual purpose of providing the necessary heat and acting as a reducing agent to remove oxygen from the iron ore. Meanwhile, a small portion of steelmaking, particularly in the US where electricity is reliable and relatively affordable, takes place in electric-arc furnaces using abundant scrap steel. While it’s a more-efficient process, it relies on natural gas.

But the most energy-intensive of all manufacturing industries is cement, according to the US Energy Information Administration. Making cement involves heating limestone to very high temperatures. Coal accounts for well over half the energy consumed in the making of cement, the main ingredient in concrete.

Hydrogen derived from renewable energy could stand in for fossil fuels in processes such as these, releasing water vapor rather than carbon dioxide as a byproduct. In steelmaking, injecting hydrogen to heat traditional blast furnaces reduces emissions by up to 20%, according to McKinsey, providing an option for producers facing the sunk costs of equipment they aren’t prepared to replace with electric-arc furnaces. And while emissions are already about 70% lower with electric-arc-furnace technology, they can be further reduced by using hydrogen as an alternative reductant to natural gas, according to US Steel, which is among industrial giants that have announced their own 2050 net-zero goal.

Hydrogen has been traditionally used as an industrial gas in much smaller quantities than what would be needed to make it the lifeblood of, say, steelmaking. Heavy industry thus presents an enormous market opportunity, even though the investments won’t be as visible to most people as the solar panels and wind turbines cropping up along highways and coasts. Based on the projects that have been announced so far, the Hydrogen Council—a group led by CEOs in the energy, industrial, and transportation sectors—estimates that total hydrogen investments will exceed US$300 billion by 2030.

To be sure, much of that investment depends on finding a cost-efficient way of getting enough renewable electricity to create hydrogen where it needs to be.

The Obstacles

Hydrogen production isn’t truly green unless the electricity used to split water molecules into hydrogen and oxygen comes from renewable sources such as solar and wind. Less than 0.1% of the world’s hydrogen is currently made this way. One setback is that the most favorable locations for solar and wind projects—places with ample sun and sustained wind, as well as plenty of space for the necessary structures—aren’t necessarily where potential industrial customers are situated.

Instead, almost all the hydrogen produced today is what’s known as grey hydrogen, which is made using fossil fuels and is used in fertilizer production and oil refining. According to a 2021 estimate by the US Department of Energy, the average cost of grey hydrogen was US$1 to US$2.50 per kilogram (kg).

The more environmentally friendly the process, the more expensive it gets. How much more expensive is difficult to pinpoint because the market for green hydrogen doesn’t yet exist. Production can be upwards of US$4 per kg by some estimates, but that’s without taking into account the considerable storage and transportation costs, given the lack of infrastructure and small number of companies skilled at handling hazardous gases—mainly industrial-gas producers such as Air Liquide and Linde.

The IRA’s tax credits can reduce production costs by up to US$3 per kg. Even though that doesn’t bridge the wide gap between green hydrogen and grey hydrogen, industry executives say laws such as the IRA are helping to resolve what they refer to as a chicken-and-egg problem: producers need access to solar and wind energy as well as customers ready to receive the hydrogen, while customers need to know they have a secure supply of the fuel at a cost-effective price before they’ll make the necessary investments. With government climate-change initiatives now incentivizing projects all along that chain, a market is finally beginning to develop. That is why, of the US$369 billion earmarked in the IRA to tackle climate change, “the incentives are particularly meaningful for hydrogen,” said Maria Lernerman, a portfolio manager for Harding Loevner’s International Carbon Transition Equity strategy.

Canada plans to enact its own proposed tax credits this year, while subsidy programs in Germany and the UK will also go into effect. In all, governments around the world have designated US$80 billion for hydrogen investments, according to a September 2022 report by the Hydrogen Council.

In the European Union, the bloc has mandated that member nations reduce greenhouse gas emissions by 55% by 2030. One way the EU is incentivizing companies to cooperate is by making it more expensive to pollute. Carbon taxes, which are levied on factories and power plants for each metric ton of carbon dioxide emitted, jumped to 100 euros per ton this year and are currently about 91 euros, up from a longstanding level of 30 euros. EU governments also reached a deal last year for the world’s biggest carbon border tax, which will apply to certain imports, such as iron and steel, and will be based on how much carbon dioxide was emitted in making the goods. The phasing out of free allowances also means that more companies will be subject to carbon taxes.

Still, the cost problem remains complex. The transition to carbon neutrality using green hydrogen will require companies to make expensive upgrades to their equipment and facilities, the kind of large capital outlays that businesses plan according to the multidecade life spans of their assets. That schedule doesn’t necessarily align with the emissions-reduction goals outlined by governments.

In the meantime, niche applications for green hydrogen are emerging, led by enterprising companies that have the financial wherewithal and operational environments to experiment with pilot projects.

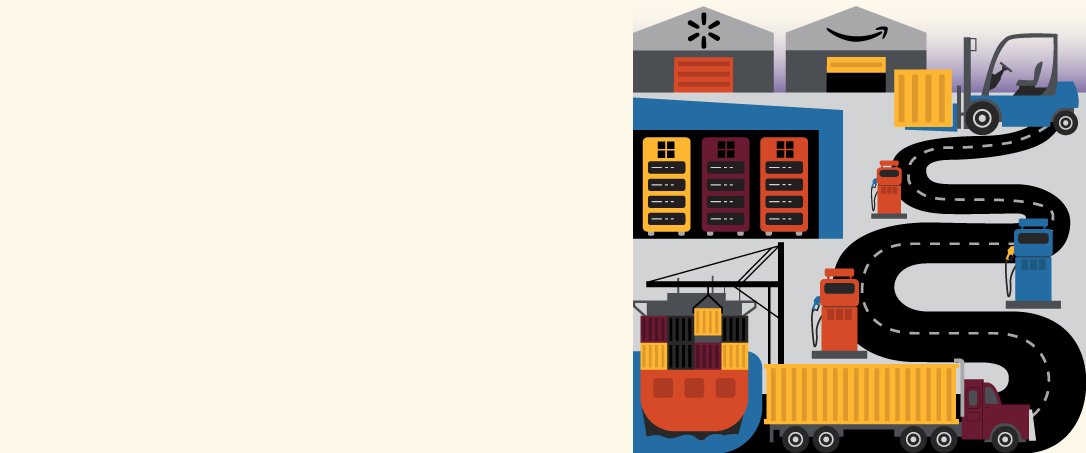

Rethinking Ports and Warehouses

When it comes to hydrogen, the distribution costs are the real killer. That’s why usage of the fuel will be confined to industrial situations in which a lot of hydrogen is consumed in one area, rather than needing to be distributed to many different refueling stations.

Shipping is one industry that offers the right conditions. The equipment used to dredge port waters of sediment and debris, the machines that unload shipping containers from ocean liners, and the heavy-duty trucks that then transport the goods could eventually use hydrogen rather than diesel.

While the same machinery could also run on batteries, the idle time needed to recharge makes batteries less than ideal for an industry that operates 24 hours a day. Bulky batteries also reduce precious cargo capacity in trucks.

In addition, long-haul trucks running on hydrogen can cover greater distances than battery-electric trucks before needing to stop, which means fewer, strategically placed refueling stations are needed along a cross-country route.

Another fleet ripe for hydrogen power is forklifts.

Amazon has 70 fulfillment centers equipped with hydrogen storage and dispensing systems, which it uses to power hydrogen fuel-cell-powered forklifts. Amazon signed a contract last year with Plug Power, a supplier of fuel cells, to provide enough green hydrogen to power 30,000 forklifts.

Walmart has used forklifts that run on hydrogen in its biggest warehouses since 2012. The company is also in the process of transitioning those to green hydrogen.

The experimentation isn’t limited to vehicles. Microsoft is planning to use green hydrogen as a replacement to backup diesel-powered generators at its data centers, for which uninterruptible power supply is crucial.

Over the last several years, Microsoft has worked with Plug Power to build a three-megawatt fuel-cell system capable of powering about 10,000 computer servers.

Present Day

For now, the largest market opportunity appears to exist within heavy industry, and the companies poised to lead the way are many of the same businesses that already work with hydrogen and substances like it. For example, Dow Chemical recently teamed up with Linde to source green hydrogen for a plant in Canada. Air Liquide last year formed a partnership with Siemens Energy to manufacture industrial-scale electrolyzers to produce green hydrogen. There are various other industrial companies operating in important niches, such as Alfa Laval, a leader in heat exchangers that supplies technology critical to achieving efficiencies along different stages of the hydrogen-production process, as well as Burckhardt Compression, a Swiss specialist in gas compression, and US-based Chart Industries, which provides liquefaction and cryogenic-storage technologies. The specialized tools and expertise needed to compress hydrogen and prevent it from deteriorating its metal surroundings creates opportunities for high-quality industrial manufacturers to provide differentiated solutions in markets with high barriers to entry.

As companies across different industries experiment with growing government support, the hydrogen future is slowly coming into view.

What did you think of this piece?

Contributors

Analysts Anix Vyas, CFA, Chris Nealand, CFA, Maria Lernerman, CFA, and Michael Purtill, CFA, and ESG Associate Maryna Arabei, CESGA, contributed research and viewpoints to this piece.

Disclosures

The “Fundamental Thinking” series presents the perspectives of Harding Loevner’s analysts on a range of investment topics, highlighting our fundamental research and providing insight into how we approach quality growth investing. For more detailed information regarding particular investment strategies, please visit our website, www.hardingloevner.com. Any statements made by employees of Harding Loevner are solely their own and do not necessarily express or relate to the views or opinions of Harding Loevner.

Any discussion of specific securities is not a recommendation to purchase or sell a particular security. Non-performance based criteria have been used to select the securities identified. It should not be assumed that investment in the securities identified has been or will be profitable. To request a complete list of holdings for the past year, please contact Harding Loevner.

There is no guarantee that any investment strategy will meet its objective. Past performance does not guarantee future results.

© 2024 Harding Loevner

Disclosures

The “Fundamental Thinking” series presents the perspectives of Harding Loevner’s analysts on a range of investment topics, highlighting our fundamental research and providing insight into how we approach quality growth investing. For more detailed information regarding particular investment strategies, please visit our website, www.hardingloevner.com. Any statements made by employees of Harding Loevner are solely their own and do not necessarily express or relate to the views or opinions of Harding Loevner.

Any discussion of specific securities is not a recommendation to purchase or sell a particular security. Non-performance based criteria have been used to select the securities identified. It should not be assumed that investment in the securities identified has been or will be profitable. To request a complete list of holdings for the past year, please contact Harding Loevner.

There is no guarantee that any investment strategy will meet its objective. Past performance does not guarantee future results.

© 2024 Harding Loevner