An unexpected interest-rate increase from the Bank of Japan helped ignite a market firestorm during the third quarter.

The central bank’s decision in late July caused a swift appreciation in the yen, a currency shift that disrupted the widely used strategy known as the yen carry trade, where investors borrowed at low Japanese rates to purchase higher-yielding foreign assets. The rapid unwinding of these positions, combined with weaker US economic data and disappointing earnings from US technology giants, culminated in a 12% drop in Japan’s Nikkei index on August 5, while expected volatility in the US equity market spiked to a level not seen outside of major crises.

Markets recovered quickly, though, and Japan ended the quarter as the second-best performing region for small-cap stocks. As the chart above shows, the yen also topped currency returns.

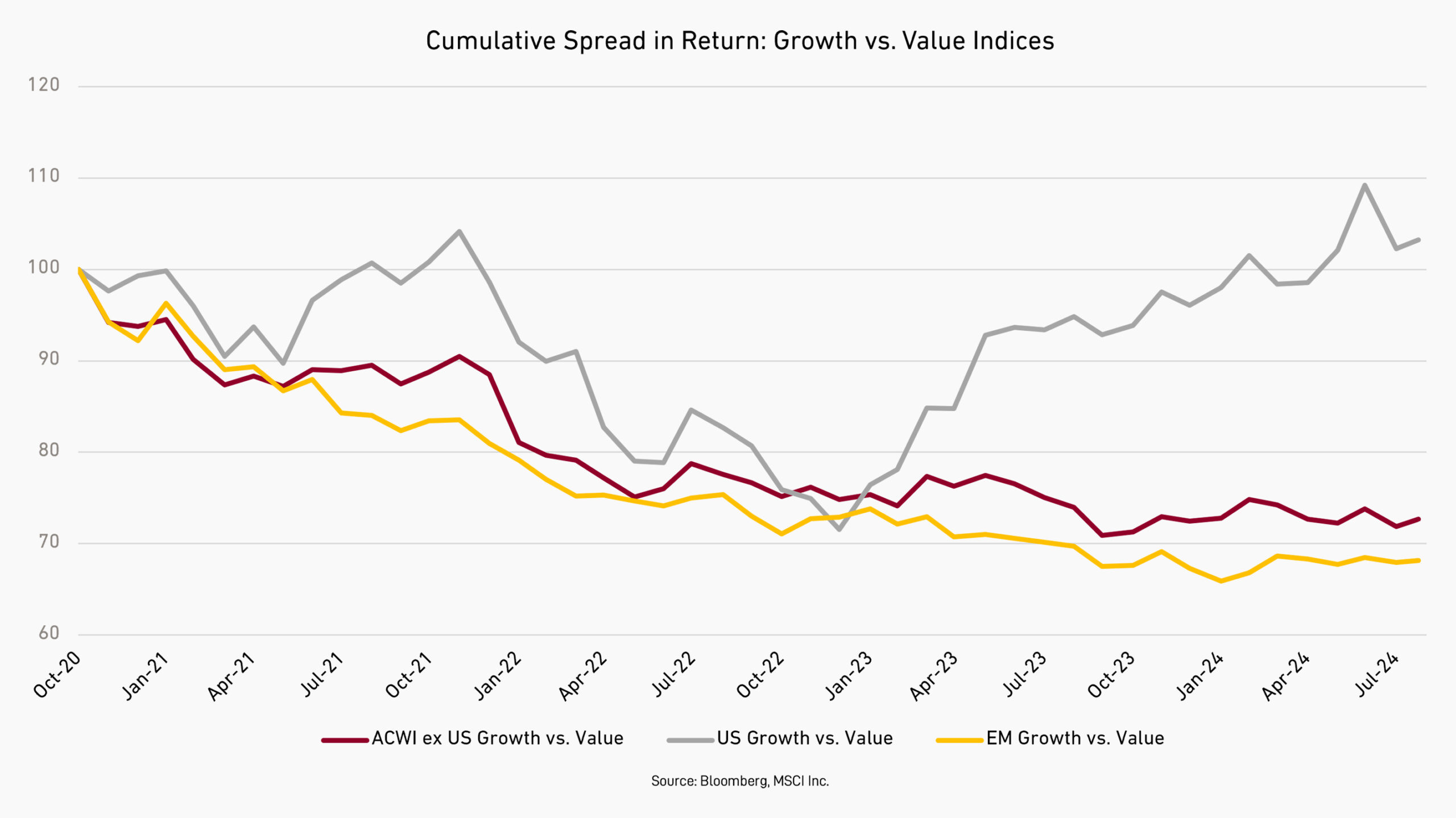

For several quarters, Japan has been a particularly challenging market for investors in quality growth small companies, as stocks of cheaper, low-quality businesses tended to outperform. However, another market development in Japan in the third quarter was that style patterns reversed, with stocks of faster-growing, more expensive companies leading returns. The charts below depict the spread between returns for the fastest- and slowest-growing, highest- and lowest-quality, and least and most expensive small caps by region for both the third quarter and trailing 12 months, based on Harding Loevner’s proprietary growth, quality, and value quintiles.

Although it’s too soon to know whether Japan’s value rally is finally over, the third quarter provided a welcome reprieve. ∎